For years, finding answers meant opening Google or YouTube, typing in a question, and sorting through a pile of articles, videos, ads, opinions, and contradictory advice.

That process is changing quickly these days and no longer really works. Search engines increasingly provide AI-generated summaries before we ever reach the original sources, and most people now just run with whatever generic answer the AI Overlords threw their way.

This creates a new problem, especially for us older adults. A generic AI response may sound polished and useful, but it is still generic. Retirement, healthcare, housing, travel, Social Security, relationships, work, and life after a career are highly personal subjects.

The right answer depends on so many factors unique to you. A broad answer written for “the average retiree” may be no more useful than a stack of search results.

The solution is not simply learning which AI button to press. It is learning how to ask better questions.

Get’cha Social Security Before You Can’t?

Ah, Social Security! Everyone’s favorite hated topic.

Now for starters, AI is not going to be the authoritative provider of “The One True Answer”. It can, however, turn a vague fear into a personalized comparison, expose the assumptions behind each option, and help you prepare better questions for Social Security or a financial professional.

Questions like:

-

Should I take Social Security at 62?

-

Am I stupid to wait when the program might change?

-

How long do I need to live before waiting pays off?

-

Will Social Security cover my basic expenses?

-

Can I stop or change my mind after claiming?

-

Is a larger guaranteed monthly check better than protecting my savings?

So how can you get a personalized answer to these and other questions?

By interacting with an AI in the way that gets results. It’s easy to forget that who you’re talking to isn’t human. It feels like a real conversation, but the nuances that people assume will be understood are not usually there. And bad assumptions can easily take you down a wrong path. Remember: spell things out, always be clear, and elaborate as much as possible to make sure your request is fully explained.

Let’s start with a basic prompt. This works with all AIs, by the way. Pick your poison (ChatGPT, Claude, Gemini, etc.) I’m going to use ChatGPT to show you how well it works for me.

I am trying to decide when to claim Social Security retirement benefits. Do not give me a recommendation yet. First, ask me one question at a time until you understand my age, estimated benefits at different claiming ages, marital situation, spouse’s benefits, work plans, essential expenses, other income, savings, health assumptions, dependents, and priorities.

After gathering the information, compare claiming at 62, my full retirement age, and 70. Show the estimated monthly and annual differences, simple break-even ages, effects of continued employment, possible effects on a surviving spouse, major risks, and the assumptions behind the comparison. Separate verified Social Security rules from general planning judgments. Identify anything that must be checked with SSA, a tax professional, or a fiduciary financial planner. Do not treat fear of future program changes as proof that I should claim immediately.

I’m going to skip the parts where I answer the questions because … well, frankly I don’t want to share my personal information with you. LOL!

The response I got back was 1200 words and quite detailed. Obviously you don’t care enough to read what it thought of my options, although I will say it was pretty accurate.

I answered the questions as I would have a year ago before I decided on early enrolment. I wanted to see what advice I would have received had I not done it the old fashioned way … pulling the trigger without much thought.

Now even you might not want to read the entire tome of results right away, so here’s a prompt that gets you closer to a real starting point:

Create a three-paragraph executive summary of the Social Security analysis you just completed. Use only the facts, estimates, priorities, and assumptions already established in our conversation.

In the first paragraph, state your primary recommendation clearly, including the claiming age you believe best fits my situation and the main reasons why. Do not hedge excessively or simply repeat that “it depends.”

In the second paragraph, explain why the other claiming ages appear less suitable, including the effects on monthly cash flow, lifetime benefits, part-time income, portfolio withdrawals, break-even ages, longevity risk, and my goal of preserving savings.

In the third paragraph, identify the most important risks, assumptions, and figures that could change the recommendation. State exactly what I should verify with my Social Security account, SSA, a tax professional, or a fee-only fiduciary financial planner before acting. Keep the complete response under 350 words, use plain language, and do not add new questions or generic background information.

Here’s what I received (sanitized):

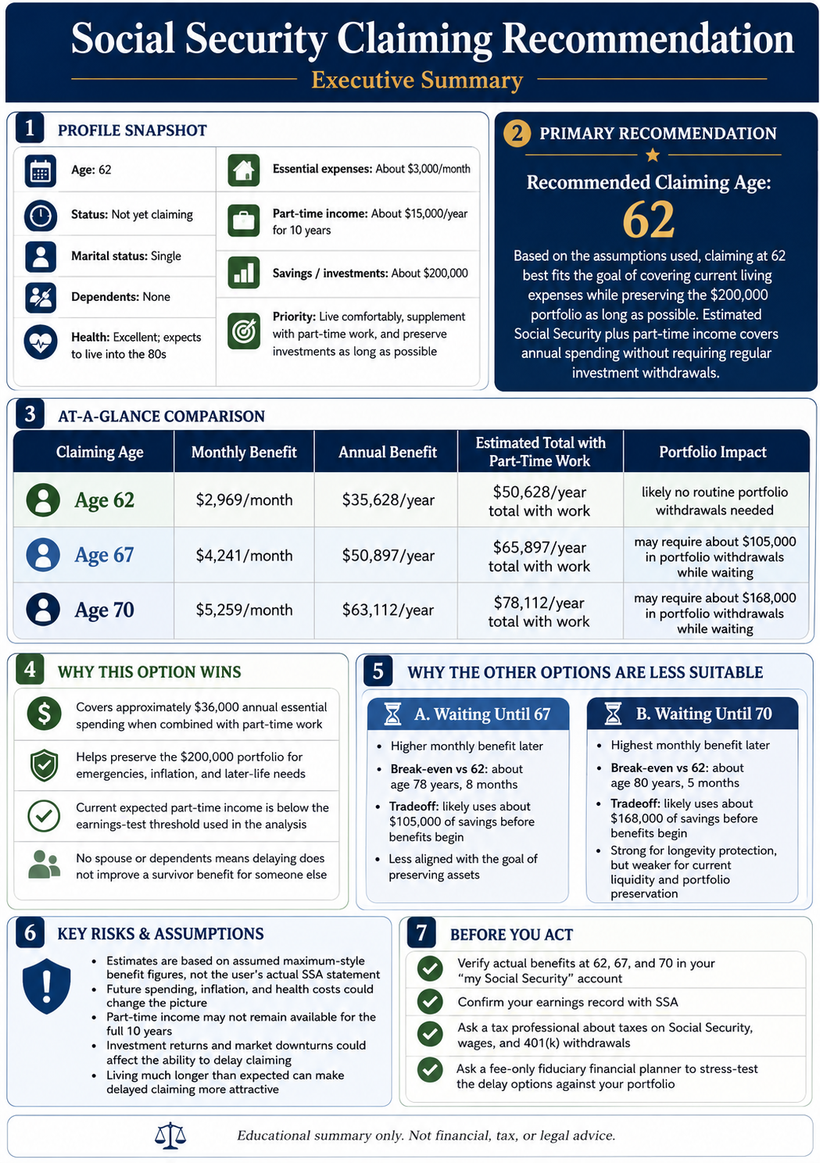

Based on the assumptions used, claiming Social Security at 62 appears to fit your situation best. Your estimated benefit of about $35,600 per year, combined with approximately $15,000 in part-time income, would cover your stated $36,000 annual living expenses without requiring regular withdrawals from your $200,000 portfolio. That preserves your investments for emergencies, inflation, major repairs, healthcare, and years when part-time work is unavailable. Because you are single with no dependents, delaying does not provide a larger survivor benefit for a spouse.

Waiting until 67 could raise your estimated benefit by roughly $1,270 per month, but covering your expenses during the five-year delay could consume about $105,000 of your investments. Waiting until 70 could produce the highest lifetime monthly benefit, but the estimated eight-year funding gap could consume roughly $168,000, leaving little financial cushion. Delaying may generate more total Social Security if you live beyond the estimated break-even ages—approximately 79 for waiting until 67 and 80 for waiting until 70—but it conflicts with your priority of preserving savings. Your expected $15,000 in annual earnings should remain below the current retirement earnings-test threshold, although that limit changes over time.

This recommendation depends heavily on estimates rather than your actual Social Security record. Before claiming, verify your personalized benefits at 62, 67, and 70 through your my Social Security account and confirm that all 35 high-earning years appear correctly. Ask SSA how your anticipated part-time earnings would affect benefits, and have a tax professional estimate the combined taxation of wages, Social Security, and possible 401(k) withdrawals. A fee-only fiduciary planner should also test whether claiming later could be supported without dangerously reducing your emergency reserves. The recommendation could change if your actual age-62 benefit is substantially lower, your expenses rise, your part-time income becomes unreliable, or your portfolio can fund the delay more safely than these simple estimates suggest.

Now even that is a bit much, although it does support my reality. I am a very visual person, so I also asked it for the results displayed in an executive infographic:

Create a clean, professional executive-summary infographic as a single image based only on the Social Security analysis we just completed.

The infographic should be designed for an older adult audience and should visually summarize the recommendation in a clear, trustworthy, easy-to-scan way. Use a polished editorial/business-infographic style, with strong hierarchy, simple icons, and readable typography. Make it feel informative rather than flashy.

Now granted only ChatGPT and Gemini can generate images, but I find that this type of information is so much easier when “snapshotted” visually.

There is obviously so much more you can do with more detailed questions, this is just a starting point. And always remember that AI works by assimilating facts it has scraped off the web, and is only as good as those facts are.

Which is obviously not perfect. “The internet said it was true, so …” is not the basis for major decisions, right?

I have been using AI for some time now in a lot of areas of my life, including retirement, travel, YouTube, and health & fitness. And the more I use it, the more I realize that the weakest link in the interaction is me. I have to be extremely clear and detailed. I need to explain exactly what I want like I would to a 5th grader. And then I have to use critical thinking to find the truth.

Ambiguity and imprecision will get you exactly what you don’t want.

Drop a comment if this helps or if you need extra help in formulating prompts. I’d love to help.

~ Rick

PS: AI responses can be wrong, incomplete, outdated, overly confident, or based on assumptions that do not apply to you. It should not replace qualified financial advisers, attorneys, doctors, tax professionals, insurance specialists, tarot card readers, or even government agencies. Important decisions should always be verified through authoritative sources and reviewed by an appropriate professional when the consequences are significant.

Never provide sensitive personal information such as Social Security numbers, account passwords, full financial account details, or private medical records unless you fully understand how the service handles that information.

There, I think that covers the legalities. Please don’t sue the messenger. LOL!